Reinventing value chains, an opportunity for Morocco

Items

China coughed and the world caught a cold. The realization of the prophetic metaphor during the covid-19 pandemic brings us back to a disenchanted reality of globalization and globalized value chains which organize the design, production and circulation of manufactured goods. Over the last thirty years, the structuring of global value chains (GVCs) has been guided by the belief that progress in logistics technologies would ensure, more and more effectively, the control of costs, deadlines and risks in value chains. dispersed over increasingly distant geographical areas.

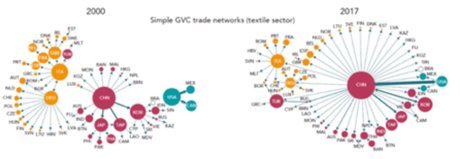

If this production model has undoubtedly made it possible, on the one hand, to free the purchasing power of consumers by reducing the cost of acquiring goods and services and, on the other hand, to ensure the economic emergence of some developing countries, it is not free from criticism. By encouraging the development of GVCs, the public policies and industrial strategies of many countries have orchestrated their dependence on major sectors such as the automobile, textiles, electronics or, more worryingly, the pharmaceutical and health industries. The Global Value Chain Development Report 2019 from the WTO and the World Bank shows how value chains have become massively structured around a central actor: China, which monopolizes more than 15% of the global export market.

The Covid-19 crisis has revealed the vulnerability of globalized logistics based on the use by major industrial powers of subcontractors or distant and often concentrated subsidiaries. Since the start of the health crisis, supply shortages supply are observed in many vital sectors. Labor-intensive industries such as automobiles, electronic components, consumer goods and textiles are particularly hard hit. In the health industry, the paralysis of Chinese production coupled with the explosion in demand for medical and protective equipment have put to the test an exceptional shock the perceptions of the fragilities and risks of supply chains globalized.

Beyond the cyclical nature of the covid-19 health crisis, we must recognize that the model based on the fragmentation of production spaces shows signs of vulnerability which contribute to the slowdown in world trade that began in 2008.

The model of extended and interdependent value chains carries structural vulnerabilities of an economic, political and societal nature.

- The rise in wage costs in Asia is no longer offset by productivity gains. Conversely, the automation and robotization of tasks reduce production costs in industrialized countries;

- Transport costs and hidden costs (defective workmanship and non-quality, delivery hazards, etc.) contribute to increasing production costs;

- The resurgence of protectionism in Europe and the United States which discourages relocation through tax, customs and non-customs measures;

- Legal provisions for controlling suppliers - such as the Sapin 2 law in France - increase the legal and financial risks linked to offshoring and cascade subcontracting;

- Finally, aspirations for new, more personalized forms of consumption and a better social and environmental impact are less and less geared towards the model of manufacturing in distant workshops that are difficult to control.

What transformation of value chains can we expect? We propose three scenarios.

Scenario 1: Business as usual

While many economists and policy makers criticize the fragilities of GVCs and the strong dependence on China, many also consider that a radical and rapid transformation is difficult to envisage. The degree of interdependence of economies and the massive investments made by companies to structure their global supply chains support the scenario of a recovery on the same bases as before the crisis.

Scenario 2: national relocation

Awareness of the loss of health sovereignty should lead to stronger intervention by States. “Defensive relocation” would be organized to secure supplies of vital goods.

However, it is unlikely that the pendulum swing will lead to a complete relocalization of production systems to the extent that major contractors will come up against two obstacles: national production capacities and the impact on the prices of manufactured goods.

Scenario 3: regional relocation

The scenario of regional relocation would be more probable and rational. This hypothesis is based on a reorganization around value chains dedicated to regional geographic markets, in which companies re-arrange their production systems and those of their partner suppliers. The establishment in a particular territory of all or part of a production sector would then depend on the conditions of attractiveness in terms of available human, material and energy resources.

While these tighter value chains allow for better supply responsiveness, they do not guarantee the resilience of the productive system. These would be favored by “redundancy” (access to additional manufacturing capacities at the risk of overcapacity), “diversity” (access to several sources of supply) and “modularity” (the ability to reconfigure a system and recombine resources) of production systems.

Regional relocation: An opportunity for Morocco?

A regional relocation - in a Euro-Mediterranean-Africa area in particular - can be an opportunity for Morocco, in terms of increasing and diversifying demand, integrating production sectors and developing innovation capacities particularly in the renewable energy and industry 4.0 sectors.

In the automotive, textile and electronic components sectors for example, Morocco could benefit from the repatriation to a Euro-Mediterranean area of part of the production currently carried out in Asia. This movement could also be accompanied by flows of Asian FDI wishing to retain their European customers by setting up in Morocco.

By illustrating the dependence of the world economy on China, the covid-19 epidemic could influence its structuring in the future. If the organization of value chains is the business of companies' industrial strategies, the health crisis shows that it is also the business of States which must protect their citizens and strengthen the resilience of their economies.

Hafsa EL BEKRI is Teacher-Researcher in international economics - Euromed Business School - Euromed University of Fez. Hicham SEBTI is a Doctor in Management from Paris-Dauphine University and Director of Euromed Business School-Euromed University of Fez.